Welcome to the ADVISORY PORTFOLIO MANAGEMENT (apm) SUMMER 2025 Quarterly Review.

The Advisory Portfolio Management (APM) Quarterly Review provides clients within the service a review of the financial world over the last three months, and how this may have affected their pension or investment. If you would like to read more about this service, please Click Here.

A key part of the reporting is the colour coding. Each APM portfolio is colour coded to enable you to spot which category applies to you. The relevant information is then presented in a clear and easy to understand way. However, if you require any further clarification, please do not hesitate to get in touch.

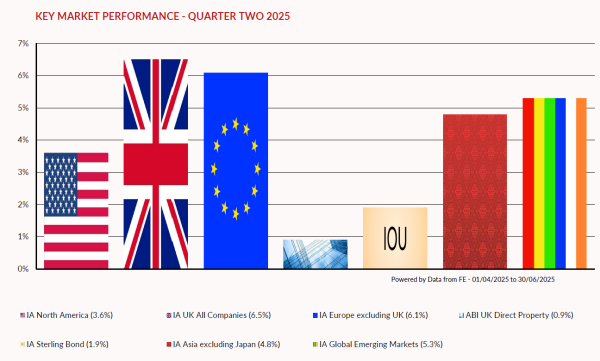

MARKET OVERVIEW – QUARTER TWO 2025

The second quarter was marked by renewed trade friction, particularly from the US, where sweeping tariffs were introduced across multiple sectors. These measures led to fears of widescale disruption to global supply chains and added to inflationary pressures, especially in Europe and the UK. Asia was particularly hard-hit, causing tensions to increase between China and the US, which led to a wider tit for tat escalation in tariffs between the two countries. Markets fell sharply, as fears of a global recession escalated, and sentiment slumped. At the height of the sell-off, US markets had fallen into bear market territory (a 20% fall), however it was the rise in US Treasury yields that caused Trump policy to pivot. Firstly, Trump announced a 90-day window to allow for countries to negotiate, which was followed later in the quarter by an agreement with China to substantially reduce the level of tariffs and allow room for a more measured discussion. Rather amusingly this led Trump to earn the nick name TACO Man (Trump Always Chickens Out). Markets needed no second invitation and rebounded strongly as the fear of a wider downturn faded, and the focus returned to the corporate earnings, interest rate cuts and consumer spending. Perhaps unsurprisingly it was the big technology stocks at the vanguard of the recovery, although defence and financials also continued to fare well.

The first half of the year has been very different, with a much more balanced cohort of companies driving returns, both at a sector and stock level. From a geographical perspective we also saw returns generated from a much broader spectrum of regions. Out of favour areas such as real estate, emerging market debt and infrastructure contributed strongly, as elevated interest rates and a falling dollar helped appetite.

As we enter the second half, the overriding theme will remain how negotiations around tariffs play out, and how far Trump is willing to push this agenda. Currently it feels that markets may be too sanguine about the outcome, so expect further pockets of volatility, however it is likely the worst is behind us. We believe the reallocation of monies away from US, driven by stretched valuations and the re-engineering of the geopolitical backdrop, will mean diversification remains key. This should mean returns being more balanced and in turn see a continuation of the outperformance from our portfolios.

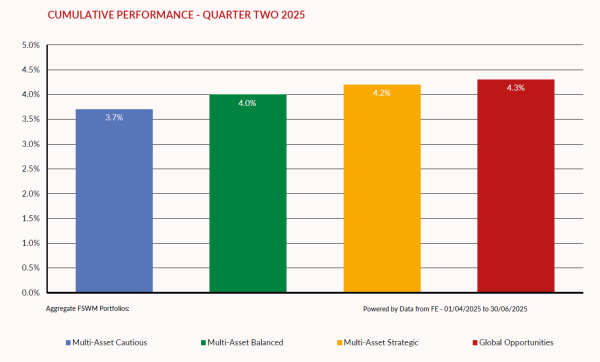

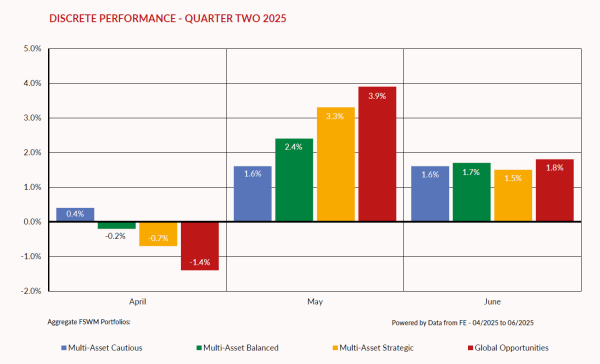

APM PORTFOLIOS – QUARTER TWO 2025 PERFORMANCE

The graphs below show how the APM portfolios within the four Finance Shop risk categories have behaved over the last three months. The first graph shows the total return for the quarter whereas the second graph illustrates the “month by month” performance. The performance figures are aggregated so, for example, the green bar is made up of all the APM Multi-Asset Balanced portfolios across all product types.

If you require specific performance figures for your plan, please contact your adviser.

PERFORMANCE REVIEW

Despite the initial sharp sell-off, all the portfolios finished the quarter in positive territory, led by the very adventurous strategy. The more diversified approach aided our returns and it was pleasing to see exposure to real assets and alternatives within the Cautious and Balanced portfolios helping to drive strong returns.

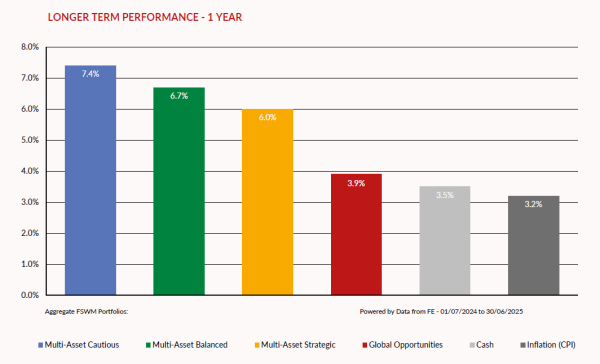

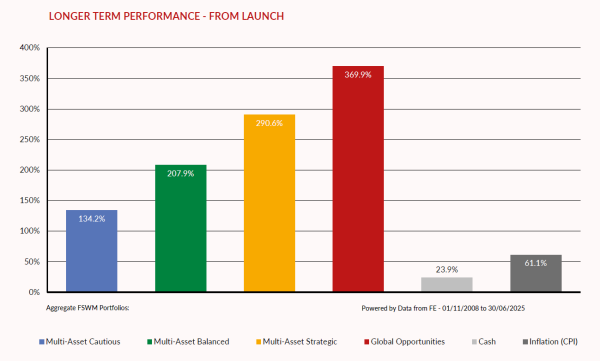

APM PORTFOLIOS – LONGER TERM PERFORMANCE

The first graph below shows how the APM portfolios have performed over 12 months. For comparison, the returns of cash (MoneyFacts 90 days’ notice 10K) and inflation (UK Consumer Price Index) are also shown. The second graph illustrates how the portfolios have performed since launch (1st November 2008).

As with the Cumulative & Discrete Performance graphs, the figures for each category are aggregated.

APM FUND REVIEW POLICY

A key part of the APM service is to monitor the underlying performance of each fund within the portfolios for both risk and return. We have selected quality funds with strong track records and therefore do not envisage a high turnover of holdings.

However, there will be occasions when the performance of an individual fund will lead to its expulsion from the portfolio(s). There are several factors that determine this decision, for example consistent under-performance, change of management team etc. It is also important, however, to have patience with a fund that is just suffering short-term under-performance.

We operate a “traffic light” system and will move a fund from a “green” to “amber” rating if the fund requires closer scrutiny at the next review. If a fund shows sufficient improvement, it will move back to “green”.

If the fund consistently under-performs without good reason its status will change to “red” and the fund will be removed from the portfolio(s). A replacement fund will be selected and all clients holding the fund within their portfolio will be notified. Upon receipt of their authority, the client’s funds will be switched accordingly.

RESULTS OF FUND & ASSET ALLOCATION REVIEW

The Investment Committee meets on a quarterly basis and one of its primary functions is to review our existing fund range.

Within this meeting we scrutinise any funds which we feel are performing significantly differently to their peer group or benchmark, with a number then run against our internal performance and risk measurements.

The funds under review are as follows:

· Atlantic House Balanced Return Fund

· Blackrock European Dynamic

· Downing Unique Opportunities

· Fidelity Strategic Bond

· Gravis UK Infrastructure Income Fund

· JP Morgan Emerging Markets Equity Fund

· Jupiter European Fund

· Liontrust Special Situations Fund

· Matthews Asia Discovery Fund

· Premier Miton UK Value Opportunities

· Regnan Global Impact Solutions Fund

· VT De Lisle America

ADDITIONAL IMPORTANT INFORMATION

This report has been issued by the Investment Committee of the Finance Shop Wealth Management team using data provided by Financial Express. Care has been taken to ensure that the information is correct but Financial Express and Finance Shop neither warrants, represents nor guarantees the contents of the information, nor does Financial Express or Finance Shop accept any responsibility for errors, inaccuracies, omissions, or any inconsistencies herein.

Past performance is not a guide to future performance. The value of investments and the income from them may go down as well as up and investors may not get back the amount originally invested. Currency fluctuations can also affect fund values. The above report does not constitute advice and you should speak to your Independent Financial Adviser before you make any alterations to investments or pension plans.

The instruments recorded above are weighted model portfolios created using Financial Express Analytics. Performance figures shown are based on the weighted models and may differ from the actual returns achieved by investors. Performance figures shown are based on bid-to-bid gross returns and do not include plan, contract, or ongoing adviser charges / commission. Please refer to your policy documentation for further details.

ABOUT FINANCE SHOP

Finance Shop is a trading name of Finance Shop Limited. Company Number 07535053. Registered in England. Registered Office: North Wood Place, Octagon Business Park, Little Plumstead, Norwich, Norfolk NR13 5FH. Finance Shop is authorised and regulated by the Financial Conduct Authority.